Can You Get GAP Insurance on a Used Car? The short answer is yes—but whether it’s available and worth buying depends on your loan, your vehicle, and the provider you choose. Many buyers assume GAP coverage is only for new cars, but a financed used car can also leave you owing more than the vehicle is worth, especially in the early years of the loan. If the car is totaled or stolen, that difference can become an unexpected out-of-pocket cost. In this guide, Life My Savings will break down how GAP insurance works for used cars, who may qualify, when it makes sense, and how to compare your options before you buy.

What Is GAP Insurance and How Does It Actually Work?

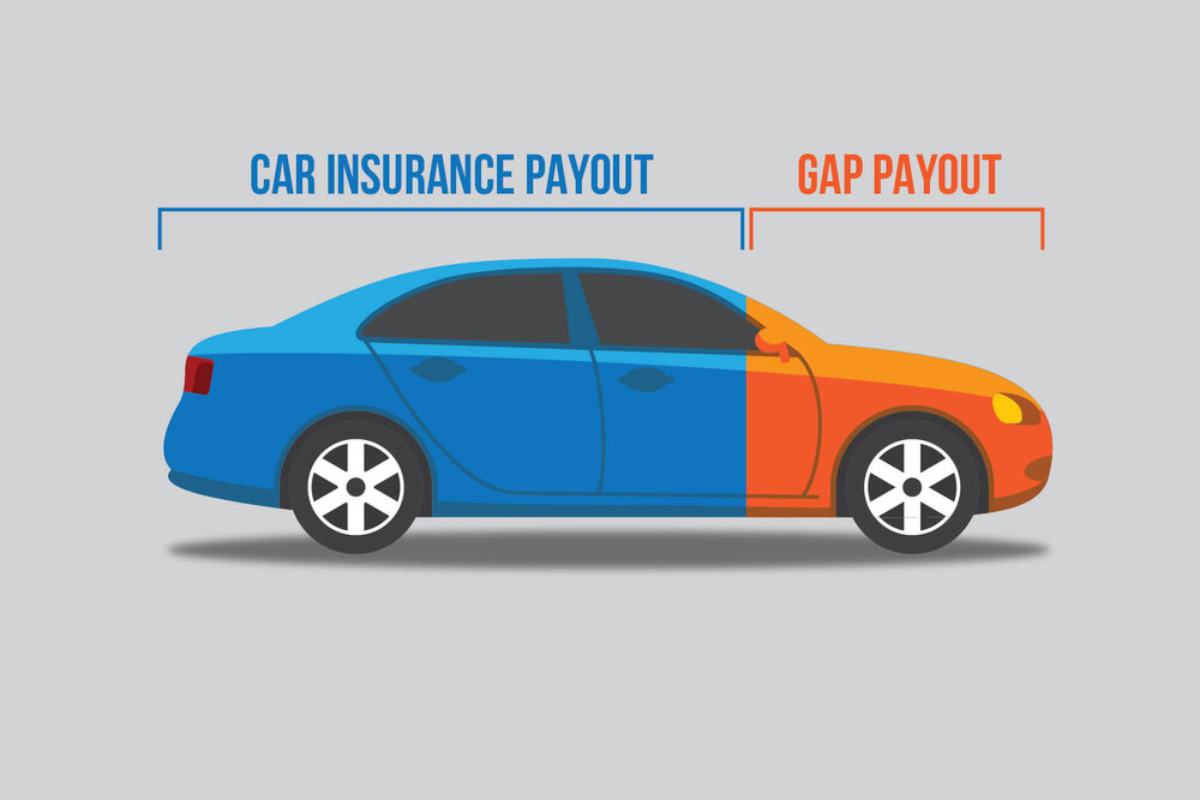

If you’ve heard the term “GAP insurance” and felt a little foggy on what it actually does, you’re not alone — it’s one of the most misunderstood auto insurance products out there. GAP coverage is designed to bridge the financial gap between what your standard auto insurance pays after a total loss and what you still owe on your car loan — a number that matters enormously when you’re dealing with the rapid depreciation of any vehicle, new or used.

Here’s how GAP coverage protects you in practice: imagine you purchased a used car and financed $18,000. A year later, the car is totaled in an accident. Your insurer assesses the vehicle’s actual cash value (ACV) at $13,500 — but you still owe $16,000 on your loan. Your standard collision policy pays out $13,500. If you want to understand that payout step more clearly, read our guide on how much insurance will pay to fix my car after a covered loss. Without GAP, you’re personally on the hook for the $2,500 difference. With GAP, that shortfall is covered, so you walk away without a lingering loan on a car you no longer own. Older drivers financing a used vehicle may also want to compare best full coverage car insurance for seniors in 2026 before deciding how much protection they need beyond basic loan coverage.

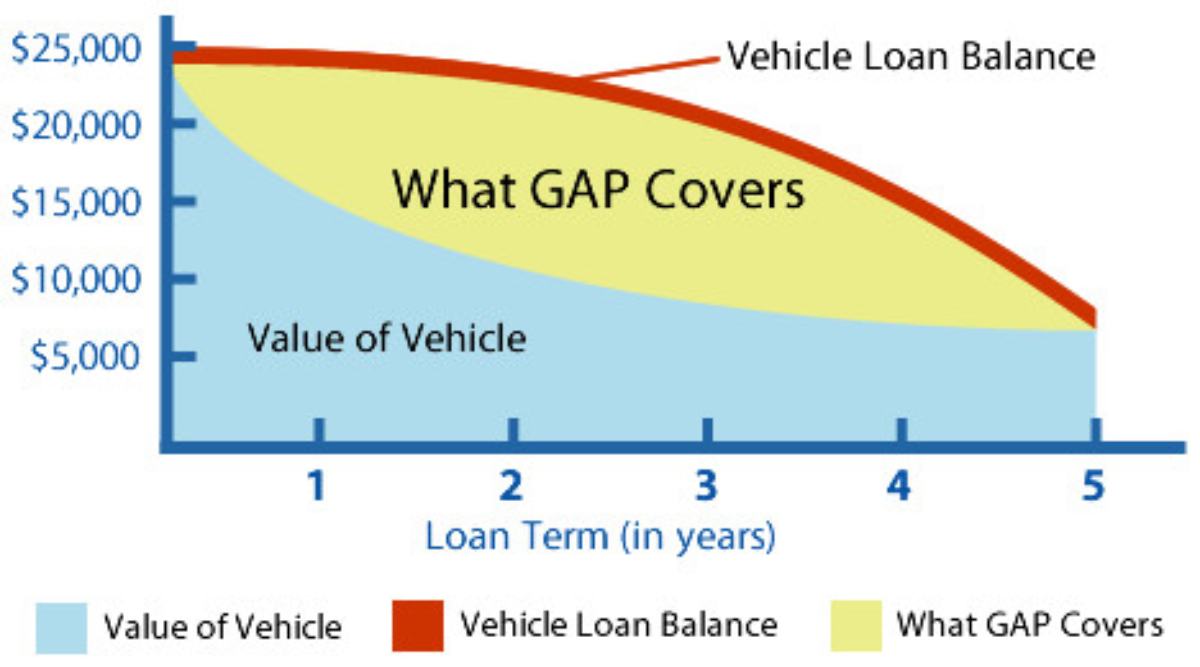

According to Investopedia and the Insurance Information Institute, GAP insurance is most valuable in the first few years of a loan when depreciation tends to outpace loan payoff — a dynamic that applies to used vehicles just as much as new ones. Vehicles can lose 10–20% of their value per year in the early years, which means even a well-priced used car can put you in a position of negative equity faster than most buyers expect.

Can I Get GAP Insurance on a Used Car?

This is one of the most common questions buyers ask — and the good news is the answer is almost always yes. The idea that GAP insurance is “only for new cars” is a persistent myth, and it can actually cost buyers real money by leading them to skip coverage they genuinely need. Whether you’re financing a certified pre-owned vehicle, a privately purchased used car, or something off a dealer lot, GAP coverage is typically available to you through multiple channels. If this purchase is replacing your previous vehicle, it may also help to understand how to switch insurance to another car before finalizing your coverage.

There are a few practical eligibility factors providers may check. The loan balance generally needs to be high enough relative to the vehicle’s actual cash value for GAP to matter. Beyond that, eligibility varies widely by provider: some insurers only cover new or nearly new vehicles or original owners, while some lenders and credit unions allow eligible used vehicles subject to age, loan, and other contract limits. In general, GAP works alongside your primary auto coverage after a covered total loss.

From a practical standpoint: if you put little to no money down on your used car, if you rolled negative equity from a previous loan into this one, or if you took out a long-term loan (72 or 84 months), there’s a very real chance your loan balance already exceeds your car’s ACV — which is exactly the scenario GAP is built for.

When Can I Use GAP Insurance? Understanding Triggering Events

A common source of confusion is when GAP insurance actually kicks in — people sometimes assume it acts like general liability coverage, but it works very differently. When you can use GAP insurance is limited to two specific triggering events: a total loss declaration by your primary insurer following an accident, or a total theft where the vehicle is never recovered.

GAP insurance does not cover partial repairs, fender-benders, mechanical breakdowns, or voluntary repossession. It also doesn’t apply if you simply decide to sell or trade in the car while underwater on the loan. The sequence of events matters: first, your primary comprehensive or collision coverage must pay out its maximum (the ACV of the vehicle, minus your deductible, depending on your policy). Only then does GAP step in to cover the remaining loan payoff amount that your primary insurer didn’t cover. If you are also wondering how long that process usually takes, it helps to review how long does it take for a car insurance claim before you rely on GAP to close the balance.

One important nuance: some GAP products may reimburse part or all of your deductible up to a stated limit, while many others do not. Always check the contract to see whether deductible reimbursement is included and, if so, how much. When comparing GAP products, that deductible inclusion clause is something to ask about specifically, because it meaningfully affects your out-of-pocket exposure in a worst-case scenario.

Should You Get GAP Insurance on a Used Car?

This is the judgment call, and the honest answer is: it depends on your financial exposure. If you are still weighing the broader financial value of stronger protection, it helps to understand how buying auto insurance helps you before settling for the cheapest option. The central question is whether you are “upside down” on your used car loan — meaning you owe more than the vehicle is worth — and if so, by how much. If you put a substantial down payment on the car, have a short loan term, and chose a vehicle known for holding its value, your loan balance may already be at or below ACV, which makes GAP less critical.

On the other hand, GAP insurance on a used car makes strong financial sense in the following situations. If you financed more than 80% of the car’s purchase price, especially with a long-term used car loan of 60 months or more, your early amortization schedule means you’re paying mostly interest for the first couple of years — which slows your equity buildup significantly. Similarly, if you rolled over a remaining balance from a previous loan (a common practice in dealer financing), you may have started the new loan already in negative equity territory. And if you’re financing a vehicle in a higher-depreciation category — think luxury sedans, pickup trucks, or high-mileage domestics — the gap between ACV and loan balance can widen faster than expected.

A useful rule of thumb from consumer finance experts: if your loan-to-value ratio at origination was above 100% — meaning your loan balance exceeded the car’s purchase price at signing — GAP insurance is a worthwhile hedge for at least the first 18 to 24 months of the loan. As you pay down the principal and the gap narrows, you can reassess whether to continue or drop the coverage.

Where Can You Buy GAP Insurance on a Used Car?

There are three main places to buy GAP insurance when purchasing a used car, and understanding the differences between them is where many buyers leave money on the table. The most expensive and least flexible option is typically through the dealership’s finance office. Dealers often bundle a GAP waiver or standalone GAP policy into the loan itself — convenient, yes, but the markup can be significant, sometimes two to three times the cost of a standalone policy. When GAP is rolled into your loan, you also pay interest on the cost of the coverage over the life of the loan.

Your existing auto insurer may be one place to look first, but products differ significantly by company. Progressive offers loan/lease payoff coverage, which is similar to GAP but capped. GEICO says its auto insurance offerings do not include GAP insurance. Allstate publishes GAP information in more than one channel, including an auto-insurance explainer and a separate vehicle-protection GAP product, so buyers should verify which product is actually available through their purchase path. Pricing varies widely by provider. When GAP is added to an auto policy, it often increases the premium by roughly $50 to $150 per year. Through a lender, dealer, or credit union, it may instead be charged as a one-time fee that can run several hundred dollars. If that fee is rolled into your loan, you may also pay interest on it over time. Timing rules vary by provider. Some products are only offered at financing or near policy inception, while some lenders and credit unions may allow GAP to be added to an existing eligible auto loan. Because enrollment windows differ, it’s best to verify the timing rules before assuming you can add coverage later.

A third option is a standalone GAP insurance provider or credit union. If your auto loan is through a credit union, GAP is frequently offered at the time of financing at a modest flat fee. Independent GAP providers also exist and can be worth comparing, especially for vehicles that don’t qualify under standard insurer criteria.

GAP Insurance vs. Other Protections: What’s the Difference?

Since many used car buyers are evaluating multiple products at once, it’s worth briefly clarifying where GAP fits relative to two frequently confused alternatives. New car replacement coverage is a different product entirely — it pays to replace a totaled vehicle with a new equivalent, rather than simply covering the loan balance. It’s generally only available on newer vehicles and doesn’t address the depreciation gap in the way GAP insurance does. If you are comparing dealer or manufacturer-linked protection products, you may also want to ask is Toyota insurance any good before choosing bundled coverage.

Loan/lease payoff coverage is similar to GAP, but it may have a payout cap and different eligibility rules. For example, Progressive says its loan/lease payoff coverage is limited to no more than 25% of the vehicle’s value, though limits vary by state. For most used car buyers with a reasonably sized loan, the distinction is minor — but if you have a large loan-to-value gap, make sure the product you’re buying doesn’t have a payout ceiling that leaves you exposed.

Extended warranties or mechanical breakdown coverage protect against repair costs and are entirely separate from GAP insurance. They’re worth discussing as a complement to GAP, not a substitute, especially on higher-mileage used vehicles.

How to Get GAP Insurance on a Used Car: Step-by-Step

Getting GAP insurance on a used car is simpler than most people expect. The process can be broken down into four practical steps, and if you already have auto insurance, you may be able to add coverage today with a single phone call or form submission.

Start by checking with your current auto insurer first and ask whether they offer GAP insurance or loan/lease payoff coverage for your vehicle. This can be one of the lower-cost options, but not always—so compare the insurer’s price, payout limits, deductible treatment, and any lender or credit-union offers before deciding. Next, gather the key information you’ll need: your current loan balance, the vehicle’s year, make, model, and mileage, and your existing coverage details. An advisor or agent will use this information to confirm your eligibility and quote a price.

If your current insurer doesn’t offer GAP on used vehicles, compare a few standalone options and check whether your loan-originating credit union or lender offers GAP at a flat fee. Avoid the dealership’s finance office unless you’ve already confirmed that the price is competitive with outside alternatives — it rarely is.

Once you’ve selected a policy, the process is typically completed in minutes: a short application, confirmation that you have comprehensive and collision coverage, and you’re covered. Many insurers allow online enrollment; others prefer a brief call. Either way, it’s a low-friction process that can protect you from thousands of dollars of exposure.

Get a Free GAP Insurance Quote — Talk to an Advisor Today

If you’ve made it this far, you’re already ahead of most used car buyers in understanding what GAP coverage is, how it works, and whether it applies to your situation. The next step is finding out exactly what GAP insurance would cost for your specific vehicle and loan — and getting personalized advice on whether your situation truly warrants it.

Fill out the short form below and one of our licensed insurance advisors will reach out to walk you through your options, compare GAP products available for your used car, and help you make a confident, informed decision. There’s no obligation, no sales pressure — just clear, expert guidance tailored to your coverage needs.

Our advisors are available Monday–Friday, 8am–6pm. Most consultations take under 10 minutes.

Frequently Asked Questions About GAP Insurance on Used Cars

Can you get GAP insurance on a used car from a private seller?

Yes, in most cases. What matters to the insurer is your loan balance relative to the vehicle’s ACV, not where you bought it. As long as you’re financing the vehicle and carrying comprehensive and collision coverage, you can typically add GAP through your auto insurer.

How long can you get GAP insurance after buying a used car?

There is no universal 30-to-45-day rule. Some GAP products must be added at financing, some insurers limit coverage to new or nearly new vehicles, and some lenders or credit unions may let you add GAP to an existing eligible auto loan. If you recently bought a used car, check your provider’s timing rules as soon as possible.

Does GAP insurance cover the deductible?

Some GAP policies include deductible coverage (usually up to $1,000); others don’t. Check the policy terms specifically — it’s a meaningful difference in out-of-pocket cost during a total loss event.

Is GAP insurance worth it on a 5-year-old used car?

It depends on your loan balance versus the vehicle’s current market value. Run the numbers: if you owe significantly more than the car is worth on the open market, GAP coverage is worth it regardless of the vehicle’s age.

When should I cancel GAP insurance on a used car?

Once your loan balance drops to at or below the vehicle’s ACV, GAP becomes unnecessary. Check your loan statement and compare it against a current vehicle valuation (Kelley Blue Book or Edmunds) every six to twelve months to know when you’ve crossed that threshold.

>>> Related Guides:

- Review should I get rental car insurance

- Learn about does credit score affect car insurance rates

- Compare how much is small business insurance for auto repair shops

William James is a personal finance and insurance writer who focuses on auto insurance, car ownership costs, and consumer-friendly coverage guides. He specializes in breaking down complex insurance topics—such as policy requirements, claims, high-risk driver coverage, and premium pricing—into clear, practical advice for everyday drivers. His work is designed to help readers compare options, understand state-specific rules, and make more confident financial decisions. At Life My Savings, William writes research-backed content aimed at making insurance and money topics easier to understand.