“Does Insurance Follow the Car or the Driver in California?” is one of the most misunderstood questions in auto insurance, especially when an accident involves a borrowed vehicle. Many drivers assume coverage automatically follows the person behind the wheel, but the rules in California are often more nuanced than that. In this guide, Life My Savings breaks down how California auto insurance works, when the car owner’s policy usually responds first, and when a driver’s own coverage may apply second.

How Car Insurance Actually Works in California

Before diving into the fine print, it helps to understand the foundation of how California auto insurance is structured — because it differs from how most people assume it works. Many drivers believe their personal policy covers them no matter which car they’re behind the wheel of, but that assumption can lead to expensive surprises after an accident.

In California, the insurance policy is tied to the vehicle first and the driver second. This principle is known as the “insurance follows the car” rule, and it’s the default framework under California auto insurance law. Older drivers who want broader protection than basic liability rules may also want to compare best full coverage car insurance for seniors in 2026 before choosing a policy. Whether you’re a policyholder, a frequent borrower of a family member’s vehicle, or someone who occasionally lets a friend drive your car, knowing this rule can protect you financially and legally.

The Primary Coverage Rule Explained

When an insured vehicle is involved in an accident — regardless of who is driving — the car owner’s liability insurance policy responds first. This is called primary coverage. The owner’s insurance company is on the hook up to the limits of the policy before any other coverage kicks in.

For example, if you lend your car to your neighbor and they cause a rear-end collision, your liability insurance pays for the damage and any bodily injury claims first. Your neighbor’s policy doesn’t come into play unless your coverage limits are exhausted.

>>> Protect your personal assets before you hand over your keys. Ensure your liability limits are high enough for California roads by [requesting a free auto insurance review today]

When the Driver’s Policy Becomes Secondary Coverage

The driver’s own auto insurance policy acts as secondary coverage — meaning it only activates once the car owner’s policy limit has been fully used. If damages exceed what the car’s policy covers, the driver’s insurer steps in to cover the remaining balance, up to the driver’s own policy limits.

This layered system (primary → secondary) is important to understand because it means lending your car is never a risk-free act, even if the person borrowing it has their own insurance.

What Does “Insurance Follows the Car” Mean in California?

This is the core principle that answers the question most California drivers are searching for, and it has direct consequences for anyone who shares a vehicle. California follows the majority rule across the United States: liability coverage is attached to the vehicle, not the person driving it.

This concept is rooted in California Vehicle Code requirements, which mandate that every registered vehicle carry minimum liability insurance. The policy covers not just the registered owner, but also anyone driving the car with the owner’s explicit or implied permission — a concept called permissive use.

Why This Matters for Liability Coverage

Liability insurance in California covers two things: bodily injury to others and property damage when you (or someone driving your car) are at fault. Because this coverage follows the car, your policy could be responsible for paying claims even when you weren’t present during the accident.

This liability exposure, however, is not unlimited under California law. California Vehicle Code §17151 places a cap on the vicarious liability of a vehicle owner in permissive-use cases — limiting that exposure to the state’s prior minimum limits (15/30/5) when the owner’s liability arises solely from permitting someone else to drive, rather than from any negligence or fault of their own.

In practice, this means your personal asset risk is most significant when the accident involves negligent entrustment — for example, if you knowingly lent your car to someone who was unlicensed, intoxicated, or had a history of dangerous driving. In that scenario, your own conduct becomes a basis for liability beyond the statutory cap, and damages could indeed threaten your personal assets. For a straightforward permissive-use situation where you simply lent your car to a responsible licensed driver, the §17151 cap provides meaningful protection.

The broader takeaway remains the same: lending your car is never entirely risk-free, and carrying coverage limits well above the California minimums is still sound advice — but the nature and extent of your exposure depends significantly on the circumstances. Consult a licensed California insurance professional or attorney for guidance specific to your situation.

When Does Insurance Follow the Driver Instead?

While the general rule in California is that insurance follows the car, there are specific situations where the driver’s policy takes precedence — or where neither policy may apply. Understanding these exceptions is just as important as knowing the rule itself.

Three main situations shift coverage responsibility to the driver rather than the vehicle, and each one carries important implications for both car owners and occasional drivers.

Named Driver Exclusions

If a car owner has explicitly excluded a specific driver from their policy — usually a household member with a poor driving record — that exclusion overrides the permissive use rule entirely. If the excluded driver gets behind the wheel and causes an accident, the car owner’s insurance will likely deny the claim.

In this scenario, the excluded driver would need to look to their own coverage — if they have a separate policy that applies. Under California Insurance Code §11580.1, a named driver exclusion is legally enforceable, meaning the car owner’s insurer can deny the claim outright. However, the exclusion itself does not guarantee the excluded driver has any other coverage to fall back on. If the excluded driver carries their own non-owner car insurance in California, that policy may provide some protection. But if they carry no separate insurance, they may face personal liability with no coverage at all — which is one of the most financially dangerous positions a driver can be in on California roads.

Non-Owner Car Insurance in California

Non-owner car insurance is a standalone policy that provides liability coverage for drivers who don’t own a vehicle but drive regularly. It acts as secondary coverage when driving a borrowed or rented vehicle and is also commonly required for drivers seeking to reinstate a suspended license or maintain SR-22 insurance in California without owning a car. If that situation applies to you, it also helps to review car insurance for a suspended license before shopping for coverage.

If you frequently borrow cars or use rideshare vehicles, non-owner coverage is worth considering — especially because it protects your personal assets if the car owner’s coverage is insufficient.

Unauthorized Use of a Vehicle

If someone takes your car without permission — whether stolen outright or taken without your knowledge — your insurance policy is generally not obligated to cover that driver. Coverage in these cases varies by insurer and policy language, so it’s always wise to review your policy’s unauthorized use clause.

Permissive Use: The Rule That Makes Borrowing Your Car Possible

One of the most important concepts in California auto insurance is permissive use, and it’s the mechanism that makes the “insurance follows the car” rule functional in everyday life. Permissive use is the insurance industry’s way of saying: if the car owner gave you permission to drive, the car’s insurance covers you.

Most California auto insurance policies include a permissive use provision, which extends the owner’s coverage to any licensed driver who operates the vehicle with consent — even if that person is not listed on the policy. This is particularly relevant for family members, friends, and coworkers who occasionally borrow vehicles.

What Counts as Permissive Use?

Permissive use can be either express (you directly said “yes, take my car”) or implied (the context makes it reasonable to assume permission was given). For example, if a family member regularly uses a car that’s kept at the home, courts may treat that as implied permission even without a formal agreement.

However, insurers can and do limit permissive use coverage. Some policies restrict the number of times or the circumstances under which a non-listed driver can use the vehicle before coverage changes. It’s worth asking your insurer specifically how your policy defines permissive use.

What If Someone Borrows Your Car Without Permission?

If a person takes your car without permission and causes an accident, your insurer may attempt to deny coverage under the unauthorized use exclusion. This scenario underscores why it’s important to be explicit and deliberate about who you allow to drive your vehicle, and to make sure unauthorized drivers cannot easily access your keys.

California’s Minimum Auto Insurance Requirements

California law requires every vehicle registered in the state to carry a baseline level of liability coverage — and understanding these minimums puts the “insurance follows the car” rule into practical context. These minimums represent the floor, not the ideal — and for many drivers, they’re dangerously low given today’s medical and repair costs.

As of the most recent California DMV and Insurance Commissioner updates, the state’s minimum liability requirements are structured to protect other drivers and pedestrians in an at-fault accident, not the policyholder’s own vehicle.

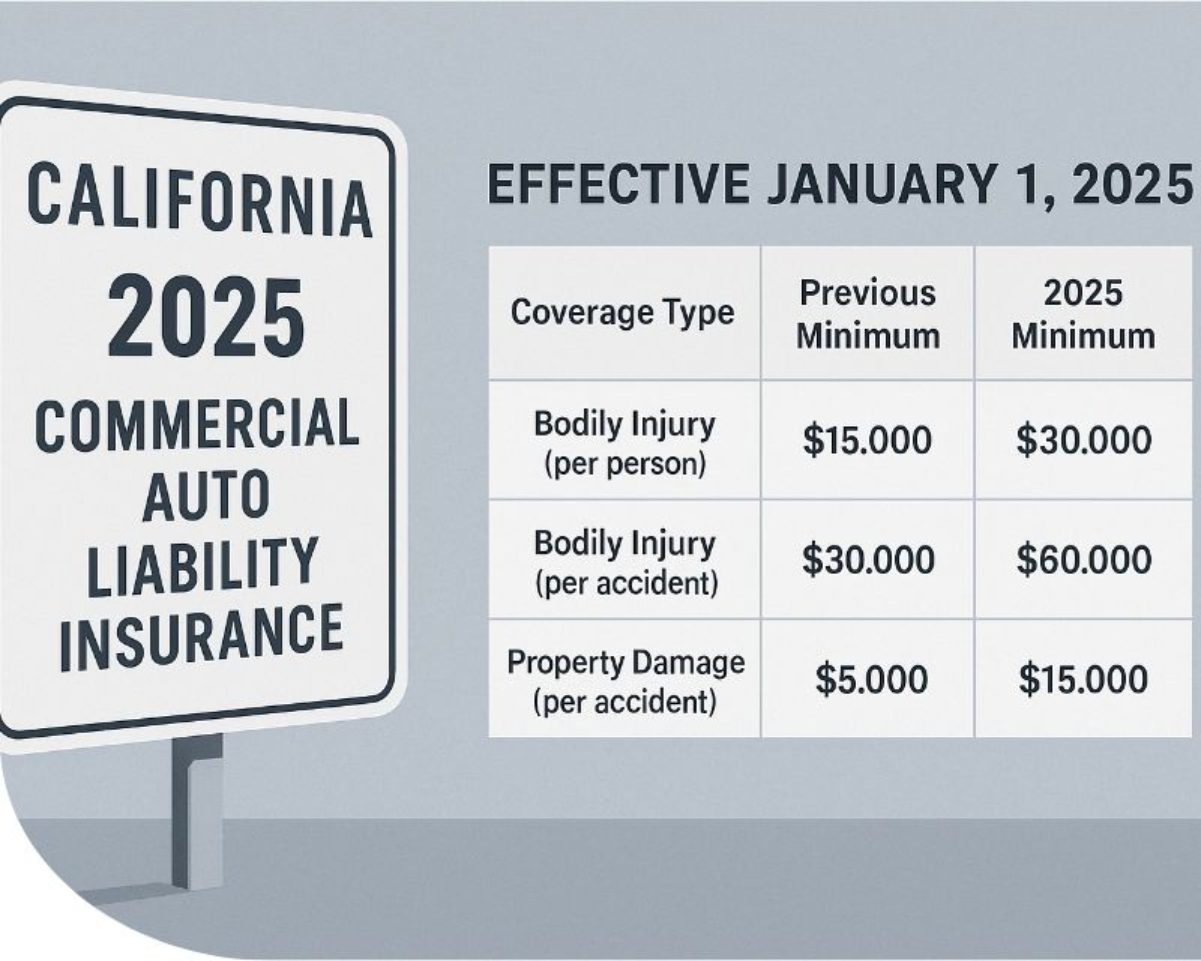

California Liability Coverage Minimums (2026)

As of January 1, 2025, California updated its minimum liability requirements under SB 1107 (signed into law in 2022):

- $30,000 per person for bodily injury

- $60,000 per accident for bodily injury (multiple people)

- $15,000 for property damage per accident

(Note: These limits increased from the long-standing 15/30/5 minimums. Always verify current requirements with the California Department of Insurance.)

These are minimums for liability only — they do not cover damage to your own vehicle. For that, you need collision coverage (damage from accidents) and comprehensive coverage (damage from theft, weather, or non-collision events). If you want the full breakdown of those updated limits, see our guide to minimum liability coverage in California.

Uninsured Motorist Coverage in California

California has one of the highest rates of uninsured drivers in the United States. According to data from the Insurance Research Council (IRC), published by the Insurance Information Institute (III), approximately 20.4% of California drivers were uninsured in 2023 — placing the state among the highest in the nation. This makes uninsured/underinsured motorist (UM/UIM) coverage an especially important add-on in California. If you’re hit by a driver without insurance, your own UM coverage compensates you for medical bills and damages that the at-fault driver can’t pay.

Real-World Scenarios: Does Insurance Follow the Car or the Driver?

Nothing makes insurance concepts clearer than walking through specific situations. These three scenarios represent the most common questions California drivers have about how insurance actually applies when vehicles change hands.

Understanding these examples gives you a practical lens for evaluating your own coverage and deciding whether your current policy is structured correctly for how you actually use your vehicle.

Scenario 1: You Lend Your Car to a Friend

Your friend borrows your car to run errands and gets into a fender-bender. Your friend has their own auto insurance policy, but yours is in force on the vehicle.

What happens: Your liability insurance responds first as the primary policy. It pays for property damage and bodily injury claims up to your policy limits. If damages exceed your limits, your friend’s insurance kicks in as secondary coverage. The claim goes on your insurance record, which could affect your future premium in California — this is one of the most underappreciated risks of lending a vehicle.

Scenario 2: You Drive Someone Else’s Car

You’re borrowing your sister’s car while yours is in the shop. You’re involved in an at-fault accident.

What happens: Your sister’s insurance policy is primary, since the car is registered to her and you’re driving with her permission under permissive use. Your own policy acts as secondary coverage. If your sister has named you as an excluded driver on her policy, her insurer may deny the claim entirely and your policy becomes primary — a situation that’s financially uncomfortable for everyone.

Scenario 3: Renting a Car in California

You rent a vehicle from a major rental company in California. You don’t purchase the rental company’s collision damage waiver (CDW).

What happens: Your personal auto insurance policy typically extends to rental cars used for personal purposes under the same terms as your regular vehicle. If you rent vehicles regularly, it may also help to review should I get rental car insurance before you decline extra coverage at the counter. Liability coverage generally follows you to the rental, and collision and comprehensive coverage also typically transfer if you carry them on your personal policy — with the same deductibles applying.

However, coverage for additional charges that rental companies may impose — such as “loss of use” fees while the vehicle is being repaired — varies significantly depending on your insurer, your specific policy language, and the terms of the rental agreement. Some policies cover these fees; many do not. Credit card rental protection programs may fill some of these gaps, but their terms also differ by card issuer and card type. The safest approach before renting a car in California is to call your insurer and your card provider in advance to understand exactly what each one covers — rather than assuming either will handle charges you haven’t verified.

How This Affects Your Auto Insurance Rate in California

Understanding who your insurance covers — and when — isn’t just academic. It has a direct impact on how California insurers calculate your premium. California uses a unique rating system because state law (Proposition 103) requires insurers to prioritize three factors: driving safety record, annual mileage, and years of driving experience.

When a claim is filed on your vehicle — even if someone else was driving — it typically appears on your claims history. Frequent borrowing by high-risk drivers can make your policy more expensive at renewal, even if you were never behind the wheel during the incident. This is one reason why many California agents recommend listing all regular drivers on your policy explicitly rather than relying on permissive use provisions.

If you own multiple vehicles or have household members with different driving histories, a multi-driver policy review is one of the most practical ways to ensure you’re not overpaying or leaving gaps in coverage.

Get a Free California Auto Insurance Quote — We’ll Call You

Not sure if your current policy has the right coverage for how you actually use your vehicle?

Whether you’re trying to understand your liability exposure when friends borrow your car, wondering if non-owner insurance is right for you, or simply looking for a better rate on your California auto insurance — our licensed agents are ready to walk you through your options.

Fill out the form below and one of our California insurance specialists will contact you within 24 hours to provide personalized advice and a free, no-obligation quote.

Frequently Asked Questions About California Auto Insurance

These are the most common questions California drivers ask about how car insurance works when multiple drivers are involved. Answering them clearly supports both your reader’s understanding and your page’s eligibility for FAQ-rich results in Google Search.

Does insurance follow the car or the driver in California?

In California, insurance follows the car as the primary rule. The vehicle owner’s liability policy covers any driver operating the car with permission. The driver’s own insurance serves as secondary coverage if the car owner’s limits are exhausted.

What happens if I let someone borrow my car and they get in an accident?

Your auto insurance becomes the primary policy and handles claims first. If damages exceed your coverage limits, the borrower’s insurance may supplement. You should be aware that the claim could still affect your future premiums, even though you weren’t driving.

Does my auto insurance cover me when I drive someone else’s car?

Yes — in most cases, your liability insurance extends to vehicles you drive with the owner’s permission, acting as secondary coverage after the car owner’s policy. If you don’t own a car at all, non-owner car insurance in California can provide standalone liability coverage.

What is permissive use in California auto insurance?

Permissive use means the vehicle owner gave another driver express or implied consent to operate their car. Under California auto insurance rules, permissive use activates the car’s primary coverage for that driver, even if they’re not listed on the policy.

Can I be excluded from someone’s car insurance policy?

Yes. A car owner can add a named driver exclusion to their policy, which removes insurance protection for a specific driver entirely. If an excluded driver operates the vehicle and causes an accident, the car owner’s insurer is likely to deny the claim.

What is the minimum car insurance required in California in 2026?

As of January 1, 2025, California requires at least $30,000 bodily injury coverage per person, $60,000 per accident, and $15,000 for property damage. These are liability minimums only and do not cover your own vehicle or injuries.

Do I need non-owner car insurance in California?

Non-owner car insurance in California is worth considering if you regularly drive vehicles you don’t own, if you need to maintain an active policy to reinstate a suspended license, or if you’re required to file an SR-22 without owning a vehicle. It provides liability coverage and peace of mind without requiring vehicle ownership.

Summary: What Every California Driver Should Know

Understanding whether insurance follows the car or the driver in California isn’t just useful trivia — it directly affects your financial exposure every time you hand someone your keys or step into a borrowed vehicle. The core rule is clear: liability coverage follows the car, the owner’s policy is primary, and the driver’s policy is secondary. But the exceptions — named driver exclusions, unauthorized use, non-owner scenarios — are where people get caught off guard.

The safest approach is to review your policy annually, list all regular drivers explicitly, carry coverage limits above the California minimums, and consult a licensed agent before any major life change that affects how your vehicle is used. If you are still comparing the bigger value of stronger protection, it helps to understand how buying auto insurance helps you before settling for lower limits.

This article is for informational purposes only and does not constitute legal or insurance advice. Coverage varies by policy, insurer, and individual circumstances. Always consult a licensed California insurance professional for guidance specific to your situation.

>>> Related Guides

- Learn how to switch car insurance to another state

- Review how to switch insurance to another car

- See whether do you need car insurance in Florida

William James is a personal finance and insurance writer who focuses on auto insurance, car ownership costs, and consumer-friendly coverage guides. He specializes in breaking down complex insurance topics—such as policy requirements, claims, high-risk driver coverage, and premium pricing—into clear, practical advice for everyday drivers. His work is designed to help readers compare options, understand state-specific rules, and make more confident financial decisions. At Life My Savings, William writes research-backed content aimed at making insurance and money topics easier to understand.