If you’ve ever asked “at what age does car insurance go down,” you’re not alone — it’s one of the most searched questions by drivers looking to lower their monthly expenses. The short answer is around age 25, but the full picture is more nuanced. Your premium doesn’t drop because of a birthday alone; it drops because insurers reassess your risk profile based on years of driving experience, accident history, and statistical patterns in claims data. In this guide, Life My Savings walk through every significant age milestone, explain how the logic works, break down the male vs. female difference, and show you what you can do right now to move toward lower rates.

Why Does Age Affect Car Insurance Rates at All?

Before diving into the specific ages when car insurance goes down, it helps to understand why age matters — because knowing the reasoning helps you take control faster.

Insurance companies use actuarial data — large-scale statistical studies of accidents, claims, and risk patterns — to predict how likely any given driver is to file a claim in a given year. Young drivers, particularly those under 25, consistently represent the highest-risk demographic on the road. According to the CDC, drivers aged 16–19 are nearly three times more likely to be involved in a fatal crash compared to drivers aged 20 and over. That elevated risk translates directly into higher premiums, because insurers are pricing in the statistical probability of a payout.

As drivers accumulate years of experience, their risk profile improves. Fewer accidents, fewer speeding tickets, and more predictable behavior all contribute to a lower expected claim cost. This is why age and driving history are among the most heavily weighted variables in any insurer’s pricing model. A clean driving record combined with reaching the right age milestones can produce some of the most significant premium reductions a driver will experience. Older drivers who are comparing stronger protection in later life may also want to review best car insurance for seniors over 70 before choosing a policy.

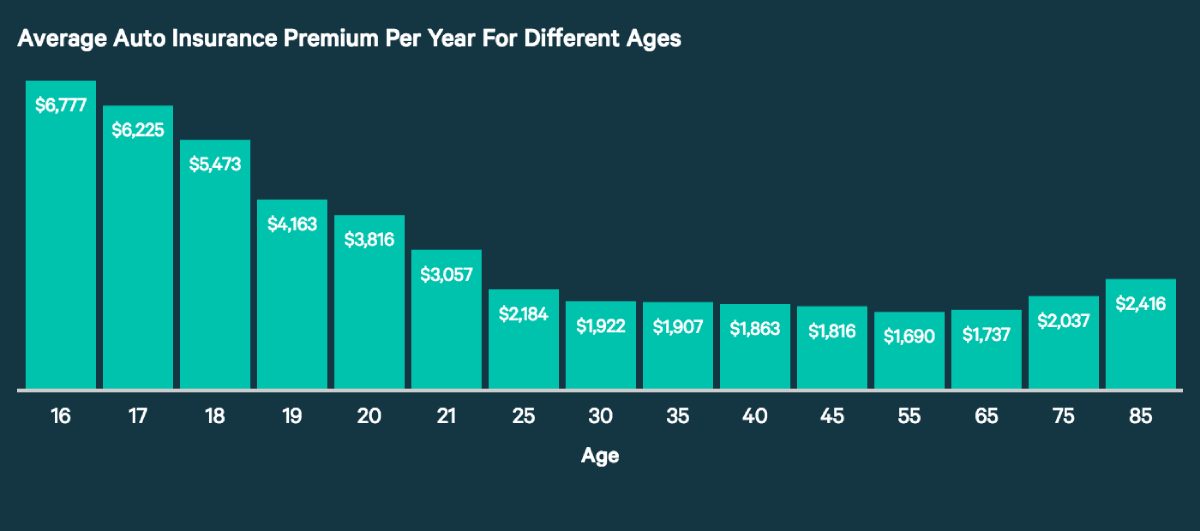

At What Age Does Car Insurance Go Down? The Key Milestones

The answer isn’t a single number — it’s a series of milestones where your insurer progressively reassesses your risk and, if your record is clean, adjusts your rate accordingly.

Age 19–21: The First Small Relief

If you completed your teen years without a major accident or violation, many insurers offer a modest rate reduction when you move out of the 16–18 age bracket. This typically isn’t a dramatic drop — around 5–10% — but it signals that the actuarial tables have shifted slightly in your favor. You’re no longer grouped with the riskiest segment of young driver pricing. If you’re still on a parent’s policy, this is also the age range where some drivers may find more competitive standalone rates as they age out of the highest-risk bracket.

Age 25: A Notable Milestone

Age 25 is widely discussed as a meaningful inflection point in auto insurance pricing, and for good reason: drivers who reach 25 with a clean record typically see a meaningful reduction in their annual premium. However, it’s worth noting that the single largest percentage drops in rates often occur earlier — particularly around ages 18–19 — as drivers move out of the highest-risk statistical bracket for the first time. By 25, insurers are classifying you as a “standard” rather than “high-risk” driver, which brings real savings, but the total reduction over your 20s accumulates gradually rather than arriving all at once.

Research from major rating bureaus suggests that the transition through your early-to-mid 20s, including the age-25 milestone, can reduce annual premiums by roughly 15–25% in aggregate for drivers with clean records, though results vary significantly by carrier and state.

Age 30–35: Steady and Reliable

By your early 30s, most insurers view you as one of their lower-risk customer segments. If you’ve maintained a consistent clean driving record through your late 20s, you’ll likely see continued modest reductions as you move through this bracket. Many discount programs — including discount availability depends more on carrier, bundling, mileage, and driving history than on age alone, as carriers actively compete for this demographic.

Age 40–60: The Lowest Rates of Your Driving Life

Statistically, drivers between 40 and 60 represent the lowest-risk group across most actuarial models. If you’ve been driving since your teens and have avoided major incidents, you’re likely approaching the lowest auto insurance rates you’ll see across your lifetime. This is the window to maximize your savings — shop your policy annually, ask about every available discount, and review whether your current coverage level still matches the value of your vehicle.

Age 65–70 and Beyond: When Rates Begin to Rise Again

Rates typically begin creeping back up for drivers in their mid-to-late 60s and beyond. While older drivers are less likely to speed or drive recklessly, they are statistically more likely to be injured in accidents and tend to file higher-value claims. Changes in vision, reaction time, and other physical factors associated with aging factor into this recalibration. That said, safe driving courses and low-mileage discounts can help meaningfully offset these increases.

Summary Table

| Age Range | Risk Level | Typical Premium Trend | Key Driver |

| 16–18 | Very High | Highest rates | Inexperience, high crash rate |

| 19–24 | High | Modest decreases (5–10%) | Experience beginning to accumulate |

| 25 | Standard | Notable reduction | 7–9 years of experience, cleaner record |

| 30–39 | Low | Further modest reductions | Established record, stable profile |

| 40–60 | Lowest | Lowest lifetime rates | Peak experience, low risk |

| 65–70+ | Moderate–High | Gradual increase | Age-related physical changes |

At What Age Does Car Insurance Go Down for Females?

Gender is one of the variables that affects when car insurance rates improve — and it produces results that are worth understanding in detail. In most states where gender-based pricing is still legally permitted, women statistically pay lower premiums than men from their very first year of driving, and that gap persists through much of their 20s.

Why Women Generally Pay Less Earlier

Statistical data from the Insurance Institute for Highway Safety (IIHS) shows that male drivers are involved in significantly more fatal accidents per mile driven than female drivers across virtually every age group. This data directly informs how insurers price policies in states that permit gender as a rating factor.

In many such states and with many carriers, female drivers tend to reach more competitive rate tiers somewhat earlier than their male counterparts with equivalent driving records — though the specific timing varies considerably by insurer, state, and individual history. It’s not accurate to name universal age thresholds here; instead, the pattern is that the gender-based premium gap tends to narrow and often largely close as both groups build experience and maintain clean records into their late 20s and 30s.

States Where Gender-Based Pricing Is Banned

As of April 2026, at least seven states — California, Hawaii, Massachusetts, Michigan, Montana, North Carolina, and Pennsylvania — prohibit the use of gender as a rating factor in auto insurance. This list may expand over time as state regulations continue to evolve; if you live in one of these states, your rate is based on other factors entirely, such as driving history, vehicle type, and annual mileage. If you want another state-specific insurance example, it also helps to review do you need car insurance in Florida before comparing requirements.

Rate Trajectory for Female Drivers

For female drivers in states that allow gender-based pricing, the overall arc looks like this: a steep starting premium at 16–18 that still tends to be somewhat lower than male peers in the same bracket, reductions through the early-to-mid 20s as experience compounds, continued improvement through the 30s and 40s, and a gradual uptick starting around the late 60s to early 70s. The lowest-cost window generally falls between ages 35 and 65.

At What Age Does Car Insurance Go Down for Males?

For male drivers, the age-rate relationship follows a similar arc but with higher starting premiums and, in states where gender is permitted as a factor, a longer period before rates reach the lowest tiers.

The Gender Gap and How It Narrows

A young male driver in his late teens or early 20s can expect to pay significantly more than a driver in his 30s with the same vehicle and coverage level — the exact difference varies widely by carrier and state. In many states and with many carriers, young men tend to pay more than young women with comparable driving records, and that gap often narrows meaningfully as both groups accumulate clean driving histories into their late 20s and 30s. The specific ages at which parity is reached are not consistent across insurers or geographies, so the best guidance is: a clean record accelerates the timeline faster than any fixed age milestone.

What Male Drivers Can Do to Accelerate the Drop

Driving record is the most powerful lever available, but it isn’t the only one. Completing a defensive driving course, driving a lower-risk vehicle, increasing your deductible, and enrolling in a usage-based insurance program — where your insurer monitors your actual driving behavior via an app or device — can all meaningfully reduce your rate before you reach the mid-20s milestone. Telematics-based programs are worth particular attention because they can help offset or reduce the impact of age-based risk pricing, depending on the insurer, which is especially valuable for young male drivers facing higher baseline rates.

Other Factors That Influence When Your Rate Drops

Age is important, but it’s far from the only determinant. Several variables interact with age to shape your final premium, and most of them are within your control.

Your driving record is the single biggest modifier. A 25-year-old with two speeding tickets and an at-fault accident may still pay more than a 22-year-old with a spotless record. Your credit score (in states where it’s permitted as a rating factor), your ZIP code, the make and model of your vehicle, your annual mileage, and the type of coverage you carry all feed into the final calculation. Drivers in larger city markets may also want to compare local rate examples like cheap car insurance in Seattle WA. If you want to understand that pricing factor more clearly, it also helps to see how credit score affects car insurance rates before comparing quotes.

The carrier you choose also matters enormously. Two insurers can look at identical driver profiles and arrive at premiums that differ by 30–40% or more, simply because they weight factors differently or are targeting different customer segments. Shopping your policy — ideally every 12 months at renewal — and comparing car insurance quotes side by side is one of the highest-return financial habits a driver can develop.

Get a Personalized Quote

Every driver’s situation is unique. Compare car insurance quotes through our tool below to see what rates are available for your age, driving history, and state — with no obligation.

Frequently Asked Questions

What age does car insurance go down the most?

The largest percentage reductions tend to occur in the late teens and early 20s as drivers exit the highest-risk statistical bracket. Age 25 is a widely cited and meaningful milestone, but it’s better understood as part of a gradual decline through your 20s rather than a single dramatic drop.

Does car insurance go down every year after 25?

Not automatically — but rates do tend to continue declining gradually through your 30s, 40s, and into your early 60s, as long as your driving record stays clean and you actively compare rates at renewal. The reductions are smaller after your mid-20s but can still add up over time.

At what age does car insurance go down for females specifically?

In states where gender-based pricing is permitted, female drivers often reach more competitive rate tiers somewhat earlier than male drivers with equivalent records, though the specific timing varies by insurer and state. In states that prohibit gender as a rating factor, this distinction does not apply.

Will my car insurance go back up after it drops?

Yes — rates typically begin rising again for drivers in their late 60s and into their 70s, reflecting changes in accident risk and claim values associated with aging. Tickets, at-fault accidents, or coverage lapses can also cause rates to rise at any age.

Can I lower my rate before I turn 25?

Yes. Defensive driving courses, usage-based insurance programs, good student discounts, staying on a parent’s policy where practical, choosing a lower-risk vehicle, and maintaining a spotless driving record are all effective strategies to reduce your premium before any age milestone arrives.

The Bottom Line

Understanding what age car insurance goes down gives you a planning framework — but the real savings come from combining that knowledge with proactive shopping and consistent safe driving behavior. The overall pattern is clear: rates are highest for new teen drivers, decline through your 20s and 30s, reach their lowest point in your 40s and 50s, and gradually increase again in your late 60s and beyond. In states that permit gender-based pricing, young women tend to reach lower-cost tiers somewhat earlier than young men, though a clean driving record is the most reliable accelerant for either group.

What matters most is not just knowing when rates should drop, but ensuring that when they do, you’re positioned with the right carrier and coverage to capture every dollar of available savings. That means comparing multiple quotes regularly, asking about every discount you qualify for, and understanding how your specific state’s rules affect your rate. If you are still comparing the broader value of stronger protection, it helps to understand how buying auto insurance helps you before settling for lower limits.

>>> Related Guides

- Review non-standard auto insurance

- See whether should I get rental car insurance

- How much is small business insurance for auto repair shops

William James is a personal finance and insurance writer who focuses on auto insurance, car ownership costs, and consumer-friendly coverage guides. He specializes in breaking down complex insurance topics—such as policy requirements, claims, high-risk driver coverage, and premium pricing—into clear, practical advice for everyday drivers. His work is designed to help readers compare options, understand state-specific rules, and make more confident financial decisions. At Life My Savings, William writes research-backed content aimed at making insurance and money topics easier to understand.