Insurers do not usually look at your regular credit score the way a bank or credit card company does. Instead, they may use a credit-based insurance score, which is built to help estimate insurance risk. This score can influence your premium, along with factors like your driving history, claims record, location, vehicle and coverage limits.

So, does credit score affect car insurance rates? In most U.S. states, yes. This Life My Savings guide explains how credit-based insurance scores work, why they may affect your premium and what you can do to make smarter coverage decisions.

Key takeaways

- Credit can affect car insurance rates in most states.

- Insurers usually use a credit-based insurance score, not your regular credit score.

- Getting a car insurance quote usually does not hurt your credit.

- Paying car insurance on time usually does not build credit.

- Some states ban or restrict credit use in auto insurance.

- If your rate is high because of credit, comparing quotes is usually the fastest way to save.

If you’re mainly trying to cut costs for a short period, it also helps to review can you pause car insurance before making changes that could trigger a lapse.

How credit affects car insurance rates

FICO estimates that about 95% of auto insurers use credit-based insurance scores in states where the practice is legally allowed. In simple terms, a higher credit-based insurance score may make you look less risky to insure. A lower score may make you look more likely to file a claim, which can increase your premium. Insurers use credit information because they believe it helps predict insurance risk.

Older drivers who want stronger protection without risking a lapse may also want to compare best full coverage car insurance for seniors in 2026 before reducing coverage too aggressively.

Still, credit does not replace driving history. If you want a broader look at how age and driving profile affect pricing, it also helps to review what age car insurance goes down. A driver with excellent credit but multiple at-fault accidents may still pay a high rate. A driver with poor credit but a clean record can still find cheaper coverage by shopping around.

Average Car Insurance Rates by Credit Score Tier (2026 Estimates)

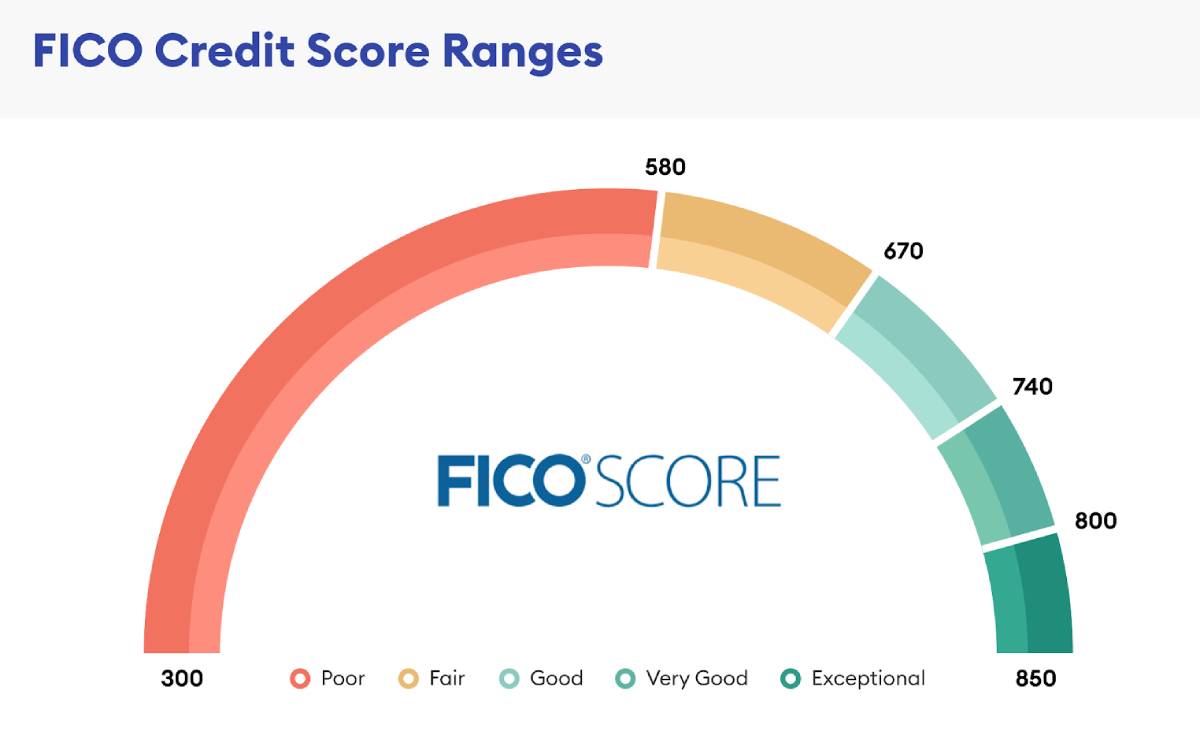

For reference, the FICO score ranges commonly used by lenders are: Poor, Fair, Good, Very Good, and Exceptional. Experian lists these ranges as 300–579 for Poor, 580–669 for Fair, 670–739 for Good, 740–799 for Very Good, and 800–850 for Exceptional.

Below is an estimated breakdown of average annual full-coverage car insurance premiums by credit tier in 2026.

| Credit / insurance score tier | FICO score range | Suggested 2026 full-coverage estimate | How it compares |

| Poor | 300–579 | $4,800–$5,800/year | Around 90%–120% higher than good credit |

| Fair | 580–669 | $3,000–$3,400/year | Around 20%–40% higher |

| Good | 670–739 | $2,300–$2,600/year | Baseline |

| Very Good | 740–799 | $1,800–$2,100/year | Around 15%–25% cheaper |

| Exceptional | 800–850 | $1,500–$1,800/year | Around 25%–35% cheaper |

These estimates are based on national full-coverage rate trends. For example, Insurance.com reports an average full-coverage cost of about $2,513 per year for a typical driver, while drivers with poor credit pay roughly $456 per month compared with about $209 per month for drivers with good credit. ValuePenguin’s 2026 analysis similarly found that poor credit can nearly double full-coverage car insurance rates.

Why your actual rate may be different

These numbers are national estimates, not guaranteed quotes. Your actual premium may be higher or lower depending on your state, ZIP code, insurer, age, driving record, vehicle, annual mileage, coverage limits, deductible, and claims history.

Also, not every state allows insurers to use credit-based insurance scores in the same way. California, Hawaii, Massachusetts, and Michigan prohibit or heavily restrict the use of credit in auto insurance pricing, while other states may limit how credit information can be used.

For the most accurate price, compare personalized quotes from multiple insurers. Even within the same credit tier, rates can vary significantly from one company to another.

Credit score vs. credit-based insurance score

A regular credit score predicts lending risk. It helps banks and lenders decide whether you are likely to repay borrowed money.

A credit-based insurance score predicts insurance risk. It uses information from your credit report, but it is built to help insurers estimate the chance of future claims or losses.

Insurers may consider credit-related factors such as:

- Payment history

- Outstanding debt

- Length of credit history

- Types of credit accounts

- Recent credit activity

However, this does not mean your income or personal background should be used to calculate the credit portion of your insurance score. Nationwide says factors such as sex, marital status, age, ethnicity, address and income are not used in its car insurance credit score calculation.

Does getting a car insurance quote hurt your credit?

No, getting a car insurance quote usually does not hurt your driving credit score.

When an insurer checks your credit for a quote, it typically uses a soft credit pull. Experian explains that car insurance quotes may involve a soft pull, but soft pulls do not affect your credit scores.

That means you can compare quotes from several insurers without lowering your credit score. If you are looking for additional quote sources, it also helps to review do credit unions offer car insurance before you compare carriers. This is important because rates can vary widely from company to company, especially if you have fair or poor credit.

States that ban or restrict credit use

Not every state allows insurers to use credit the same way.

California, Hawaii, Massachusetts and Michigan are commonly listed as states that ban or heavily restrict the use of credit in auto insurance pricing. Bankrate also notes that these states prohibit or limit credit as a rating factor for auto insurance.

Other states may allow credit use but place limits on how insurers apply it. Because insurance rules are state-specific, check your state insurance department for the most current rule where you live.

Does paying car insurance build credit?

Usually, no. Paying your car insurance premium on time helps keep your policy active, but it typically does not build your credit score.

Liberty Mutual explains that car insurance payments do not build credit because insurance premiums are not reported to credit bureaus the way loan or credit card payments are.

However, missed payments can still cause problems. If your policy is canceled for nonpayment and you still owe a balance, the unpaid amount may be sent to collections. The CFPB says credit reporting companies can generally report negative payment history for up to 7 years.

So, if you switch insurers, do not simply stop paying. Before canceling too casually, it also helps to understand what happens if you don’t pay car insurance and how a lapse can affect your record. Cancel your old policy properly and confirm whether you owe any remaining balance.

What if a life event hurt your credit?

If your credit dropped because of a major life event, ask your insurer whether it offers a reconsideration process.

Some insurers may review your situation if your credit was affected by events such as:

- Divorce

- Death of a spouse, parent or child

- Serious illness or injury

- Temporary involuntary job loss

- Military deployment

- A government-declared disaster

Nationwide lists several extraordinary life circumstances that may qualify for premium reconsideration, including divorce, serious illness, job loss and overseas military deployment.

You may need to provide documentation, but it is worth asking if the event directly affected your credit.

How to lower car insurance rates with poor credit

If poor credit is increasing your car insurance rate, start with the actions that can help fastest.

First, compare quotes from at least 3 insurers. Each company weighs credit differently, so the cheapest insurer for 1 driver may not be the cheapest for another.

Next, ask for discounts. Common discounts include safe driver, bundling, autopay, paperless billing, low mileage, defensive driving and telematics programs.

Then, review your credit reports for errors. AnnualCreditReport.com states that free weekly online credit reports are available from Equifax, Experian and TransUnion.

You can also improve your credit over time by paying bills on time, lowering credit card balances, avoiding too many new accounts and disputing inaccurate credit report information.

Improving credit may not lower your premium immediately. Many insurers review credit at renewal or when you request a new quote.

Frequently Asked Questions (FAQ)

1. What is a good credit score for car insurance?

Generally, a credit score of 700 or higher is considered “good” for car insurance purposes and will help you secure below-average rates. If your score falls into the “Very Good” or “Exceptional” tiers (750 to 800+), you will unlock the most competitive discounts available. While insurers use proprietary credit-based insurance scores rather than traditional FICO scores, maintaining a standard FICO score above 700 almost always translates to a strong insurance score.

2. Does credit score affect car insurance in California?

No. If you live in the Golden State, your credit score has absolutely zero impact on your car insurance rates. Under California’s Proposition 103, auto insurers are legally banned from using credit history to price policies or deny coverage. Instead, your rates are determined by three primary factors: your driving safety record, the number of miles you drive annually, and your years of driving experience.

3. Does credit score affect car insurance in Michigan?

Yes, but with strict limitations. Michigan has unique laws regarding insurance pricing. State regulations prohibit auto insurers from using your standard “credit score” directly. However, they are allowed to use your “credit information” (like your payment history) to generate a proprietary insurance score. Even then, an insurance company in Michigan cannot deny you coverage, cancel your policy, or base your premium solely on your credit history.

4. How rare is a 796 credit score?

A 796 credit score is very impressive. On the standard FICO scale (which ranges from 300 to 850), a 796 falls comfortably into the “Very Good” category and is just four points shy of being “Exceptional.” While it isn’t extremely rare—roughly 20% to 25% of Americans have a score of 800 or above—it is significantly higher than the national average, which hovers around 715. With a 796 credit score, you pose very little risk to insurers and will easily qualify for the best possible car insurance rates in states that allow credit-based pricing.

Credit can affect car insurance rates in most U.S. states, but it is not the only factor. Insurers usually use a credit-based insurance score, not your regular credit score. Getting a quote should not hurt your credit, and paying your premium usually will not build credit. If your rate is high, compare quotes, ask about discounts, check your credit reports and review your options before your next renewal. If you want a broader explanation of why the right protection matters beyond just price, it also helps to review how buying auto insurance helps you.

Ready to see if you are overpaying? Compare car insurance quotes today and find a policy that fits your budget.

>>> Related Guides

- Review can you have 2 insurance policies on the same car

- Learn how long can you stay on your parents car insurance

- Compare how much is small business insurance for auto repair shops

William James is a personal finance and insurance writer who focuses on auto insurance, car ownership costs, and consumer-friendly coverage guides. He specializes in breaking down complex insurance topics—such as policy requirements, claims, high-risk driver coverage, and premium pricing—into clear, practical advice for everyday drivers. His work is designed to help readers compare options, understand state-specific rules, and make more confident financial decisions. At Life My Savings, William writes research-backed content aimed at making insurance and money topics easier to understand.